Day 22: The Security Base Class

Engineering a type-safe, memory-efficient abstraction for every tradeable asset in the engine.

Contents

1. The “Fat Dataclass” Trap

Junior engineers — and most tutorial code you will find online — model a security like this:

# DON'T DO THIS

security = {

"symbol": "AAPL",

"price": 182.5000000000002, # float arithmetic gift

"fractionable": True,

"option_strike": None, # None for equities — why is this field here?

"crypto_network": None, # likewise

"tradable": True,

}

Sometimes it graduates to a dataclass with 30 fields and 12 Optional[...] annotations. Same problem. You add CryptoPerp support six weeks later, forget to implement margin_requirement(), and the gap between “it compiled” and “it blew up in production” is exactly one leveraged trade.

This is not a hypothetical. Real money disappears this way. The abstraction boundary you build today is the wall between a systematic edge and account ruin.

2. The Failure Mode: Three Silent Killers

None of these failures shout at you. They accumulate quietly — in your P&L, in your memory, in your first 3 AM incident.

Killer 1 — Float Price Drift

>>> tick = 0.01

>>> price = 182.50

>>> price % tick

7.105427357601002e-15 # should be 0.0

Your tick-violation check passes because 7e-15 is not zero but is also not caught as an error. The broker rejects the order. You never see the failure — it lands in an async callback you forgot to handle. The order is silently dropped.

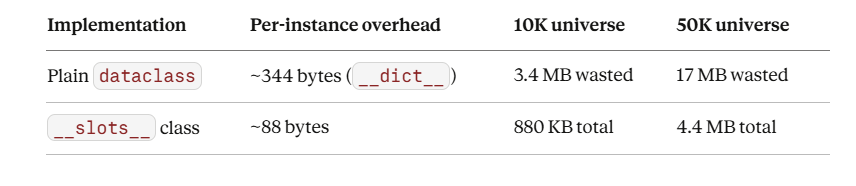

Killer 2 — Memory Bloat at Universe Scale

Without __slots__, every Python instance carries a __dict__. For 10,000 securities in a universe scan:

This is before you attach market data. At 50,000 symbols — the full US equity universe — the difference is 13 MB of dead weight the GC must clean up on every tick cycle.

Killer 3 — Structural Incompleteness

No abstract base class enforcement means CryptoPerp.margin_requirement() is silently missing until your risk engine calls it. Python’s duck typing will not save you here — the attribute access will succeed, the method will not exist, and you will get an AttributeError in the middle of a volatility spike. The abstract contract is the last line of defense.

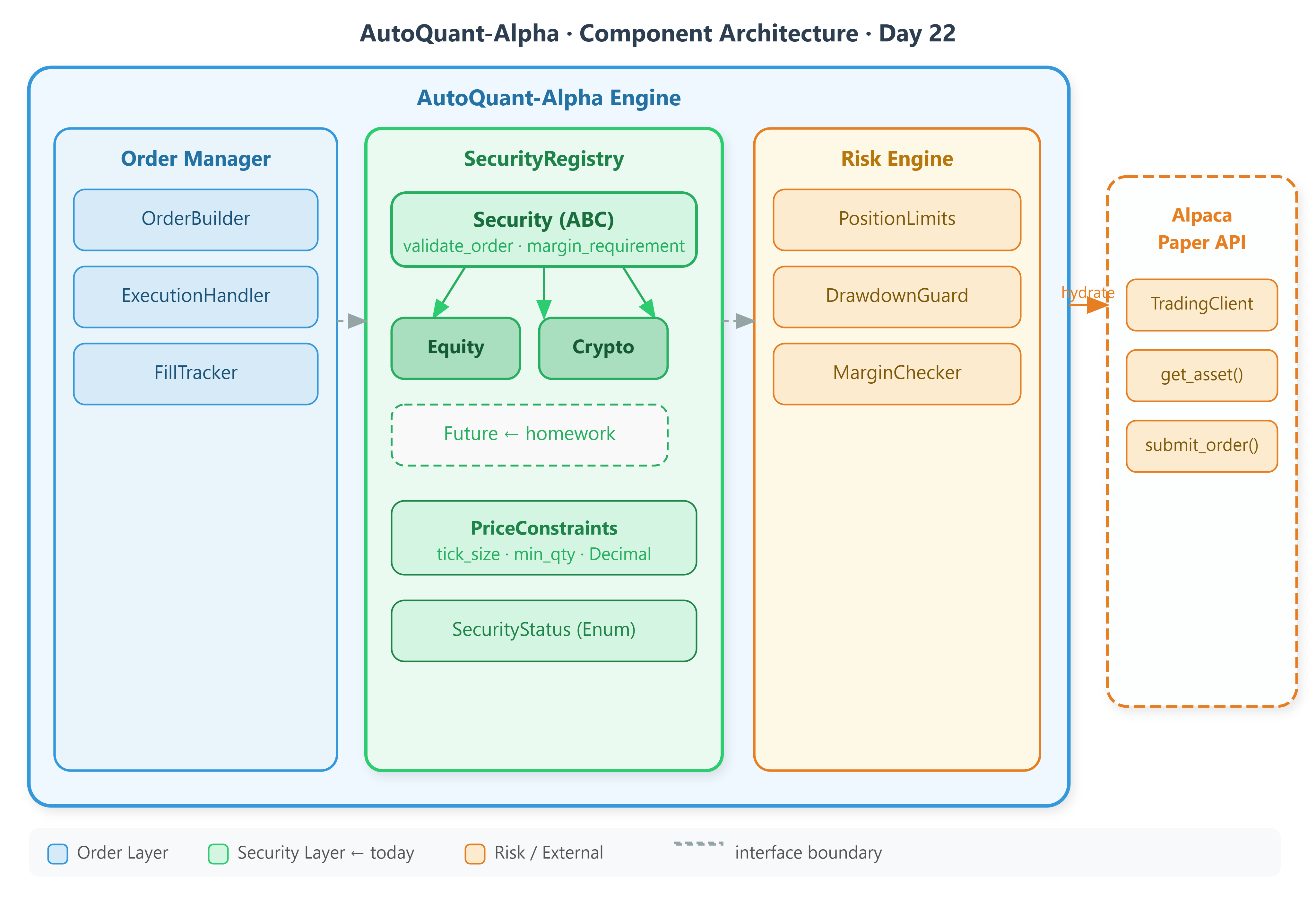

3. The AutoQuant-Alpha Architecture

We build three tightly coupled components. Each layer has exactly one responsibility and no knowledge of the layers above it.

PriceConstraints (frozen dataclass, Decimal arithmetic)

└─ Security (ABC, __slots__, @abstractmethod enforcement)

├─ Equity (NYSE / NASDAQ / OTC)

├─ Crypto (Spot, Alpaca BASE/QUOTE format)

└─ Future (homework — CME Globex)

└─ SecurityRegistry (thread-safe singleton + Alpaca hydration)

The invariants enforced at construction time are non-negotiable:

Symbol is normalized — uppercase, non-empty, valid charset per asset class.

Prices are

Decimal, neverfloat. The type system is the first validator.Tick size is stored as

Decimalfor exact modular arithmetic.Status is a typed

Enum— not a string you can typo at 2 AM.