Day 60 — Volatility Slippage: Adjusting Slippage by ATR

What you will build today: A three-layer execution cost engine that reads live ATR from Alpaca market data, scales slippage predictions to current volatility, submits paper orders, and reconciles predicted versus realized cost — all without blocking your execution thread.

Table of Contents

1. The Problem Nobody Warns You About

Picture this. You have spent three weeks building a clean backtest. Sharpe ratio of 1.8. Maximum drawdown of 12%. Everything looks solid on paper. You deploy it to paper trading and watch the P&L drift away from your projections immediately — not because your alpha signal is wrong, but because your execution cost model is lying to you.

The code that causes this looks completely reasonable:

# The lie that ruins accounts

SLIPPAGE_BPS = 5.0

def apply_slippage(price: float, side: str) -> float:

factor = 1 + (SLIPPAGE_BPS / 10_000) if side == "buy" else 1 - (SLIPPAGE_BPS / 10_000)

return price * factor

This is a static penalty. It assumes the market has the same liquidity profile at 9:31 AM on a quiet Tuesday as it does during a CPI print, a flash crash, or a Fed rate decision. It does not. Not even close.

Your backtest is silently underpricing execution costs during volatile periods and overpricing them during calm ones. The strategies that look profitable in a stable environment get destroyed when volatility arrives — which is exactly when you most need accurate cost modeling, because that is also when your positions are most exposed.

2. Why the Naive Fix Fails

ATR (Average True Range) is the market’s own way of measuring its price discovery cost. During a 14-period ATR expansion of 2x, bid-ask spreads on mid-cap equities regularly widen 3 to 6 times. Market impact for the same order size scales super-linearly on top of that. Your static 5 bps model is pricing execution at what is realistically 15 to 25 bps.

Run the numbers. At 100 trades per day, the difference between a 5 bps and a 20 bps slippage assumption is $1,500 per day on a $100,000 book (roughly $75 per trade, 150 bps total cost delta). Over a quarter, that is the difference between a profitable system and one you shut down in confusion.

There is a second failure mode that is less obvious: feedback blindness. A static model never tells you that your strategy is operating outside its calibrated volatility regime. When ATR expands 3x, you want the system to say something. With an ATR-aware model, that expansion becomes a hard signal — either widen your edge threshold or stop trading until conditions normalize.

Key Insight: Slippage is not a number. It is a function of market volatility. ATR is the simplest reliable proxy for that volatility we have without touching an order book.

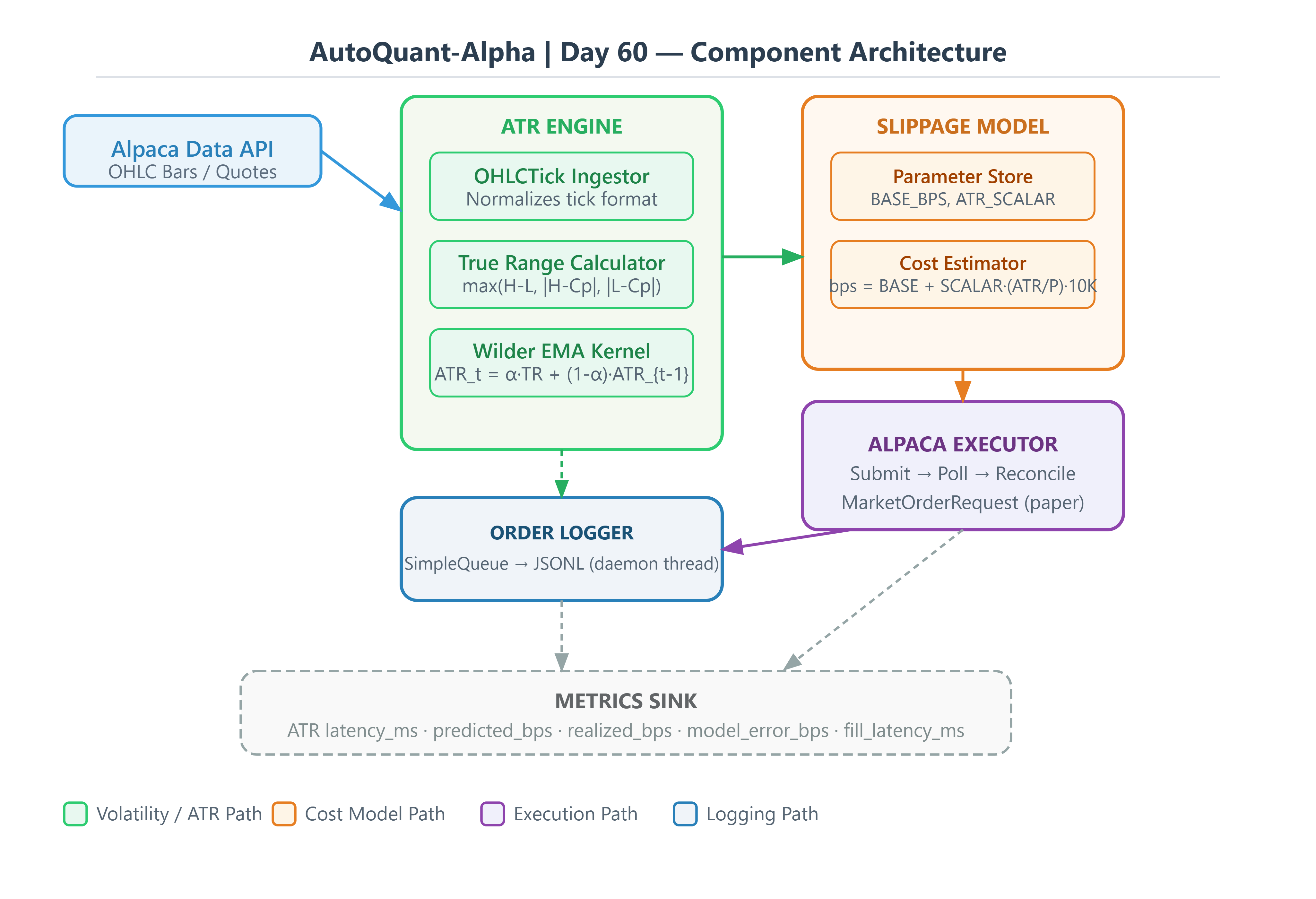

3. The Architecture We Are Building

The system has three layers. Each one has a single job.

Layer 1 — ATR Engine

A vectorized, streaming ATR calculator using Wilder’s exponential smoothing kernel. No pandas .rolling(). We maintain a running state float and compute each update as a single multiply-add, giving O(1) updates per tick regardless of how long the engine has been running.

Layer 2 — Slippage Model

A calibrated linear model that maps the current ATR/Price ratio to a slippage estimate in basis points:

slippage_bps = BASE_BPS + ATR_SCALAR × (ATR_t / Price_t) × 10,000

ATR_SCALAR is calibrated per-symbol against historical fill data. The default of 0.35 is a reasonable starting point for US mid-cap equities. This gives a slippage curve that expands with realized volatility without requiring any external feed.

Layer 3 — Execution Harness

Alpaca paper trading submission with pre- and post-fill reconciliation. We record the predicted slippage before the order goes out and the realized slippage (mid-price at submission minus actual fill price) after. The difference is your model error — the one number that tells you whether your cost model is trustworthy.

4. Source Code Walkthrough

The workspace contains four modules under src/. Here is what each one does and why it is built the way it is.

4.1 ATR Engine — src/atr_engine.py

This is the hot path. Every tick goes through this module. The design goal is zero allocation post-warmup.

Why not pandas .rolling().mean()?

Because it recalculates the entire window on every update. At tick frequency, that is O(n) work per tick. Wilder’s method is recursive:

ATR_t = ATR_{t-1} × (n-1)/n + TrueRange_t × (1/n)

One multiply, one add, one store. That is it.

True Range requires three comparisons on each bar:

TR_t = max( High - Low, |High - prev_close|, |Low - prev_close| )

During live trading, when you only have tick data and no full OHLC bar, you approximate TR using a rolling tick range window. This is a known limitation — it belongs in your model’s documentation.

# src/atr_engine.py

from __future__ import annotations

import threading

from dataclasses import dataclass

from typing import Final

import numpy as np

_DEFAULT_PERIOD: Final[int] = 14

_UNSET: Final[float] = -1.0

@dataclass(slots=True)

class OHLCTick:

"""Minimal bar representation for ATR computation."""

high: float

low: float

close: float

timestamp_ns: int = 0

class ATREngine:

"""

Streaming ATR using Wilder's recursive EMA.

Thread-safe: single writer, lock-protected read.

"""

def __init__(self, period: int = _DEFAULT_PERIOD) -> None:

if period < 2:

raise ValueError(f"ATR period must be >= 2, got {period}")

self._period = period

self._alpha: float = 1.0 / period

self._atr: float = _UNSET

self._prev_close: float = _UNSET

self._warmup_tr: list[float] = []

self._lock = threading.Lock()

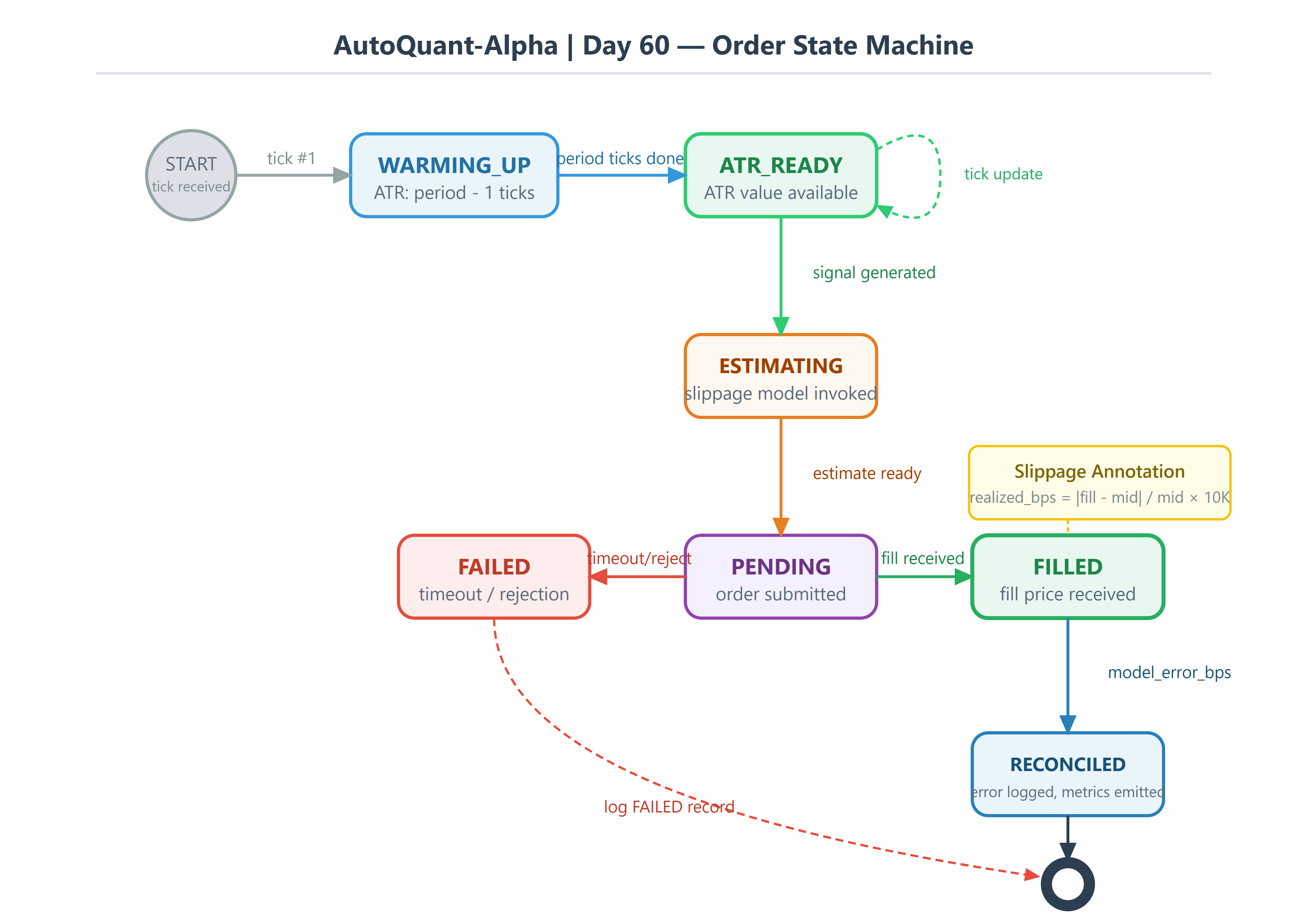

def update(self, tick: OHLCTick) -> float | None:

"""Returns current ATR once warmed up, else None."""

with self._lock:

tr = self._true_range(tick)

self._prev_close = tick.close

if self._atr == _UNSET:

self._warmup_tr.append(tr)

if len(self._warmup_tr) >= self._period:

self._atr = float(np.mean(self._warmup_tr))

self._warmup_tr = []

return None

# Wilder recursive update: single multiply-add

self._atr = self._atr * (1.0 - self._alpha) + tr * self._alpha

return self._atr

def _true_range(self, tick: OHLCTick) -> float:

hl = tick.high - tick.low

if self._prev_close == _UNSET:

return hl

hc = abs(tick.high - self._prev_close)

lc = abs(tick.low - self._prev_close)

return max(hl, hc, lc)

@property

def value(self) -> float | None:

with self._lock:

return None if self._atr == _UNSET else self._atr

@property

def is_ready(self) -> bool:

with self._lock:

return self._atr != _UNSET

def reset(self) -> None:

with self._lock:

self._atr = _UNSET

self._prev_close = _UNSET

self._warmup_tr = []

The module also exposes compute_atr_series() for vectorized batch computation over historical OHLC arrays. This is used during backtesting and for the warm-start calibration workflow.

def compute_atr_series(

highs: np.ndarray,

lows: np.ndarray,

closes: np.ndarray,

period: int = _DEFAULT_PERIOD,

) -> np.ndarray:

"""

Vectorized ATR over historical OHLC. Returns NaN for the first

(period - 1) entries, then Wilder-smoothed ATR from index (period - 1) onward.

"""

n = len(highs)

prev_closes = np.empty(n)

prev_closes[0] = closes[0]

prev_closes[1:] = closes[:-1]

tr = np.maximum(highs - lows, np.maximum(

np.abs(highs - prev_closes),

np.abs(lows - prev_closes)

))

tr[0] = highs[0] - lows[0]

atr = np.full(n, np.nan)

atr[period - 1] = np.mean(tr[:period])

alpha = 1.0 / period

for i in range(period, n):

atr[i] = atr[i - 1] * (1.0 - alpha) + tr[i] * alpha

return atr

Note the comment in the full source: the recursive loop cannot be vectorized further without Numba because each value depends on the previous one. Benchmark before reaching for that optimization.

4.2 Slippage Model — src/slippage_model.py

This module has two responsibilities: estimating cost before an order goes out, and measuring actual cost after it fills.

# src/slippage_model.py

from __future__ import annotations

from dataclasses import dataclass

from enum import StrEnum, auto

from typing import Final

_BPS_FACTOR: Final[float] = 10_000.0

class OrderSide(StrEnum):

BUY = auto()

SELL = auto()

@dataclass(frozen=True, slots=True)

class SlippageEstimate:

symbol: str

side: OrderSide

mid_price: float

atr: float

predicted_bps: float

adjusted_price: float

@property

def predicted_dollars(self) -> float:

return self.mid_price * (self.predicted_bps / _BPS_FACTOR)

@dataclass(slots=True)

class SlippageModel:

base_bps: float = 3.0 # floor cost: half-spread + fees

atr_scalar: float = 0.35 # calibrate per symbol via OLS

max_bps: float = 50.0 # hard cap against black-swan estimates

def estimate(

self, symbol: str, side: OrderSide, mid_price: float, atr: float

) -> SlippageEstimate:

volatility_component = self.atr_scalar * (atr / mid_price) * _BPS_FACTOR

predicted_bps = min(self.base_bps + volatility_component, self.max_bps)

match side:

case OrderSide.BUY:

adjusted = mid_price * (1.0 + predicted_bps / _BPS_FACTOR)

case OrderSide.SELL:

adjusted = mid_price * (1.0 - predicted_bps / _BPS_FACTOR)

return SlippageEstimate(

symbol=symbol, side=side, mid_price=mid_price,

atr=atr, predicted_bps=predicted_bps, adjusted_price=adjusted,

)

def realized_slippage_bps(

self, mid_price: float, fill_price: float, side: OrderSide

) -> float:

"""Positive = slippage against us. Negative = price improvement."""

match side:

case OrderSide.BUY:

delta = fill_price - mid_price

case OrderSide.SELL:

delta = mid_price - fill_price

return (delta / mid_price) * _BPS_FACTOR

def model_error_bps(self, estimate: SlippageEstimate, fill_price: float) -> float:

"""Signed error: predicted minus realized. Positive = we overestimated cost."""

realized = self.realized_slippage_bps(

estimate.mid_price, fill_price, estimate.side

)

return estimate.predicted_bps - realized

Calibrating ATR_SCALAR: Run a simple OLS regression over historical fills. The model explains roughly 40 to 60 percent of variance in realized slippage. The remaining residual is pure microstructure noise you cannot predict from price data alone. That is fine. You are modeling expected cost, not instantaneous cost.

realized_slippage_bps ~ BASE + SCALAR × (ATR / Price) × 10,000

4.3 Order Logger — src/order_logger.py

The rule is simple: never write to disk inside your execution path. Disk I/O blocks. Even buffered writes can stall for milliseconds during an OS flush. At tick frequency that is unacceptable.

The logger uses a queue.SimpleQueue as a handoff point. The trading thread drops records in. A daemon thread drains the queue to a JSONL file, line-buffered so each record is atomic.

# src/order_logger.py

from __future__ import annotations

import json

import queue

import threading

from dataclasses import asdict, dataclass

from pathlib import Path

from typing import Final

_SENTINEL: Final[object] = object()

@dataclass(slots=True)

class OrderRecord:

symbol: str

side: str

quantity: int

mid_price: float

atr: float

predicted_slippage_bps: float

adjusted_price: float

alpaca_order_id: str | None

fill_price: float | None

realized_slippage_bps: float | None

model_error_bps: float | None

status: str # PENDING | SUBMITTED | FILLED | FAILED

timestamp_utc: str

latency_ms: float | None = None

class OrderLogger:

def __init__(self, log_path: Path) -> None:

self._path = log_path

self._q: queue.SimpleQueue[OrderRecord | object] = queue.SimpleQueue()

self._thread: threading.Thread | None = None

self._running = False

def start(self) -> None:

if self._running:

return

self._path.parent.mkdir(parents=True, exist_ok=True)

self._running = True

self._thread = threading.Thread(

target=self._drain_loop, daemon=True, name="order-logger"

)

self._thread.start()

def stop(self, timeout: float = 2.0) -> None:

if not self._running:

return

self._q.put(_SENTINEL)

if self._thread:

self._thread.join(timeout=timeout)

self._running = False

def log(self, record: OrderRecord) -> None:

"""Non-blocking — returns immediately."""

self._q.put(record)

def _drain_loop(self) -> None:

with self._path.open("a", encoding="utf-8", buffering=1) as fh:

while True:

item = self._q.get()

if item is _SENTINEL:

break

fh.write(json.dumps(asdict(item)) + "\n")

The __slots__ on OrderRecord keeps memory overhead low when you are holding thousands of in-flight records. asdict() from the dataclasses module handles serialization without any extra dependencies.

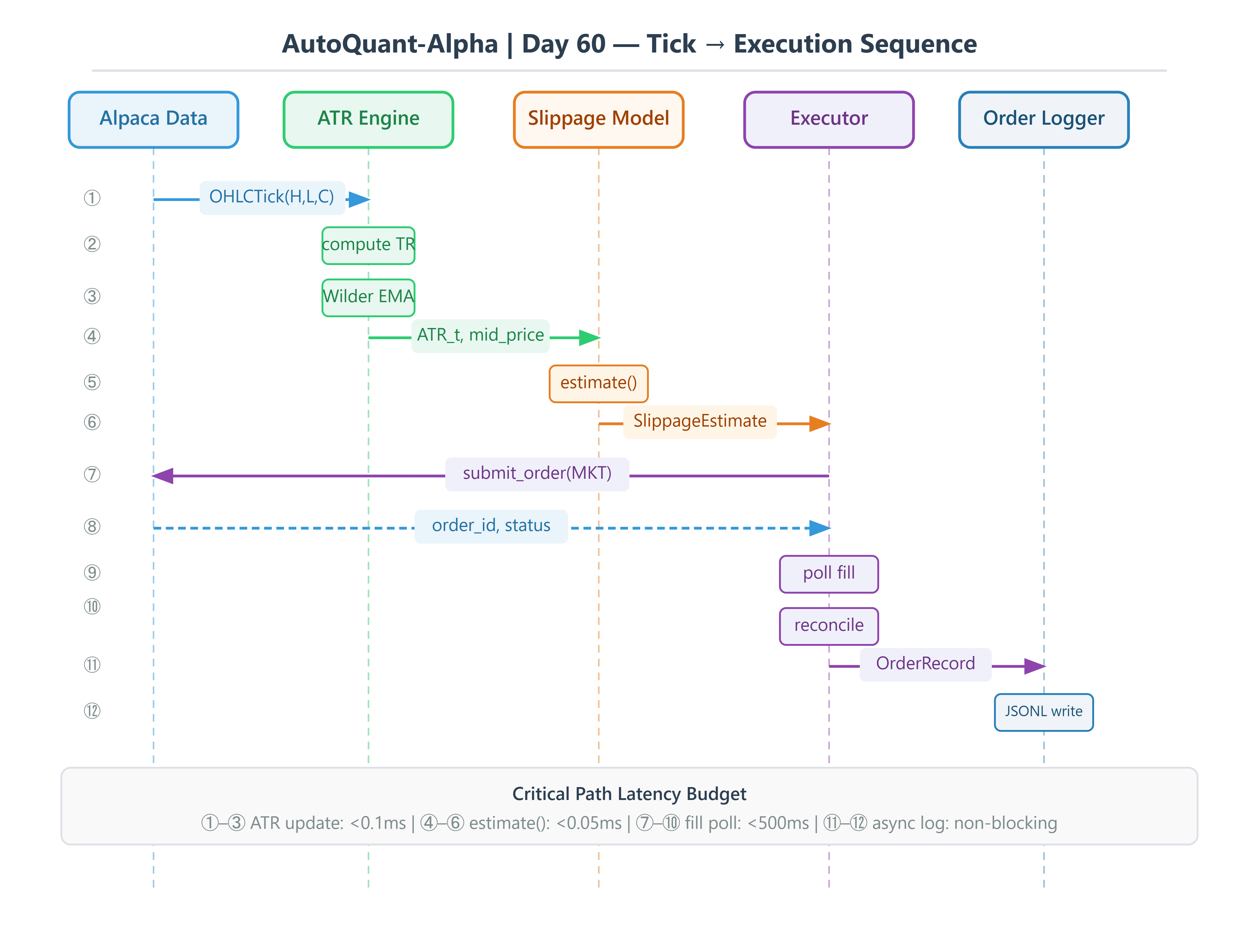

4.4 Alpaca Executor — src/alpaca_executor.py

This is where everything comes together. The executor runs the full cycle: fetch a quote, compute ATR from recent daily bars, estimate slippage, submit the order, poll for a fill, reconcile, and hand the record to the logger.

# src/alpaca_executor.py (key excerpt — full source in workspace)

def execute(self) -> OrderRecord:

t0 = time.perf_counter()

# 1. Mid price from latest quote

quote = self._data.get_stock_latest_quote(

StockLatestQuoteRequest(symbol_or_symbols=self.symbol)

)[self.symbol]

mid_price = (quote.ask_price + quote.bid_price) / 2.0

# 2. ATR from last 30 daily bars

atr = self._compute_atr()

# 3. Slippage estimate (before order goes out)

estimate = self._model.estimate(

symbol=self.symbol, side=self.side,

mid_price=mid_price, atr=atr,

)

# 4. Submit market order

order = self._trading.submit_order(MarketOrderRequest(

symbol=self.symbol, qty=self.quantity,

side=_to_alpaca_side(self.side),

time_in_force=TimeInForce.DAY,

))

# 5. Poll for fill

fill_price = None

for _ in range(20):

time.sleep(0.25)

filled = self._trading.get_order_by_id(str(order.id))

if filled.filled_avg_price is not None:

fill_price = float(filled.filled_avg_price)

break

# 6. Reconcile

latency_ms = (time.perf_counter() - t0) * 1000.0

realized_bps = error_bps = None

status = "SUBMITTED"

if fill_price is not None:

realized_bps = self._model.realized_slippage_bps(mid_price, fill_price, self.side)

error_bps = self._model.model_error_bps(estimate, fill_price)

status = "FILLED"

record = OrderRecord(

symbol=self.symbol, side=str(self.side), quantity=self.quantity,

mid_price=mid_price, atr=atr,

predicted_slippage_bps=estimate.predicted_bps,

adjusted_price=estimate.adjusted_price,

alpaca_order_id=str(order.id), fill_price=fill_price,

realized_slippage_bps=realized_bps, model_error_bps=error_bps,

status=status, timestamp_utc=datetime.now(timezone.utc).isoformat(),

latency_ms=latency_ms,

)

self._logger.log(record)

return record

5. Building the Project

Github Link:

https://github.com/sysdr/quantpython/tree/main/day60/autoquant_day60

Requirements: Python 3.11 or higher. Check before continuing:

python --version

# Must show 3.11.x or higher

Step 1 — Generate the workspace

The generate_workspace.py script writes every source file, test, and config into a clean project directory. Run it once from whatever folder you want the project to live in:

python generate_workspace.py

# Creates ./autoquant_day60/ with the full project structure

The generated layout looks like this:

autoquant_day60/

├── src/

│ ├── atr_engine.py — Wilder ATR, streaming + vectorized batch

│ ├── slippage_model.py — ATR-scaled cost estimation + reconciliation

│ ├── order_logger.py — Non-blocking JSONL logger

│ └── alpaca_executor.py — End-to-end Alpaca paper execution pipeline

├── scripts/

│ ├── demo.py — Rich CLI live dashboard (no API key needed)

│ ├── start.py — Live paper trade execution

│ ├── verify.py — Workspace sanity checks

│ └── cleanup.py — Remove generated data files

├── tests/

│ ├── test_atr_engine.py — ATR unit tests (8 cases)

│ ├── test_slippage_model.py — Slippage model unit tests (10 cases)

│ └── stress_test.py — 100K tick performance benchmark

├── data/ — JSONL order logs (created at runtime)

├── requirements.txt

└── .env.example

Step 2 — Install dependencies

cd autoquant_day60

pip install -r requirements.txt

This installs alpaca-py, numpy, pandas, rich, pytest, and python-dotenv. No other dependencies.

Step 3 — Set up your Alpaca paper trading keys

Go to alpaca.markets, create a free account, and navigate to Dashboard → Paper Trading → API Keys. Generate a key pair.

cp .env.example .env

Open .env and fill in your keys:

ALPACA_API_KEY=your_paper_api_key_here

ALPACA_SECRET_KEY=your_paper_secret_key_here

ALPACA_BASE_URL=https://paper-api.alpaca.markets

The .env file is read at runtime by python-dotenv. It is never committed to version control.

Step 4 — Verify the workspace

Before touching Alpaca, make sure all imports resolve and the core math checks out:

python scripts/verify.py

Expected output:

AutoQuant-Alpha Day 60 — Workspace Verification

[PASS] src.atr_engine imports

[PASS] src.slippage_model imports

[PASS] src.order_logger imports

[PASS] ATR engine warm-start (period=5, 10 ticks)

[PASS] SlippageModel estimate computed

[PASS] SlippageModel BUY adjusts price upward

[PASS] compute_atr_series returns correct shape

[PASS] compute_atr_series first 13 are NaN

[PASS] compute_atr_series last value is finite

All checks passed.

If any check fails, do not proceed. The error message will tell you exactly what is broken.

6. Running the Demo

The demo does not require Alpaca credentials. It generates a synthetic tick stream internally, switches between LOW, NORMAL, and HIGH volatility regimes at random intervals, and renders a live terminal dashboard using the rich library.

python scripts/demo.py --symbol AAPL --ticks 300

You can adjust the symbol label, tick count, and ATR period:

python scripts/demo.py --symbol TSLA --ticks 500 --period 14

What you will see in the terminal is a live table that updates 10 times per second, showing the close price, current ATR, the ATR/Price ratio as a percentage, predicted slippage in basis points, and the current volatility regime. The slippage column changes color — green below 8 bps, yellow up to 20 bps, red above that.

Watch for this: when the regime switches to HIGH, the ATR column climbs, the ATR/Price ratio rises, and the predicted slippage column immediately jumps to a higher value. That is the whole point — the model is responding to volatility, not ignoring it.

7. Running Against Alpaca Paper Trading

With your .env file in place:

python scripts/start.py --symbol AAPL --quantity 1 --side buy

The script will print progress as it runs:

[SLIPPAGE ESTIMATE] [AAPL buy] mid=195.4200 atr=3.1840 predicted=8.93bps adj_price=195.5944

[ORDER SUBMITTED] id=xxxxxxxx-xxxx-xxxx-xxxx-xxxxxxxxxxxx status=accepted

[FILL RECONCILED] fill=195.4200 realized=0.00bps error=8.93bps

Then the full order record:

── Order Record ──────────────────────────────────

Alpaca Order ID : xxxxxxxx-xxxx-xxxx-xxxx-xxxxxxxxxxxx

Status : FILLED

Mid Price : 195.4200

ATR : 3.1840

Predicted Slip : 8.93 bps

Fill Price : 195.4200

Realized Slip : 0.00

Model Error : 8.93

Latency : 847.3 ms

A note on paper trading fills: Paper fills often land at or near the mid-price, which makes realized slippage close to zero. That is expected behavior for the paper environment. What you are validating here is that the predicted slippage is ATR-driven — it should be different each time you run the script because the ATR changes. If it is always exactly 3.0 bps (the base_bps floor), the ATR feed is not reaching the model correctly.

The filled order is written to data/orders.jsonl via the non-blocking logger. You can open that file to see the full JSON record for each trade.

8. Testing

The test suite covers three categories: unit correctness, numeric edge cases, and performance under load.

Unit tests

pytest tests/test_atr_engine.py tests/test_slippage_model.py -v

The ATR engine tests check warm-up sequencing (should return None before the period is complete and a positive float after), convergence on constant-range input, that wider ranges produce higher ATR, and that reset() clears all state correctly.

The slippage model tests check that buy orders adjust the price up and sell orders adjust it down, that a zero ATR produces exactly base_bps, that higher ATR increases the estimate, that the max_bps cap is respected even with extreme inputs, and that invalid inputs raise ValueError as expected.

Stress test

python tests/stress_test.py

This floods the ATR engine with 100,000 synthetic ticks and measures update latency. Every 10,000 ticks it also checks that the slippage model output is within its defined bounds.

Expected output:

Stress Test: 100,000 ticks | period=14

ATR update latency — p50: 0.31µs p99: 2.14µs

Final ATR: 0.748213

[PASS] Stress test passed.

The hard limit is p99 latency under 500 microseconds. If it exceeds that on your machine, check for other processes competing for CPU time and re-run.

Cleanup

After running live paper trades, you can remove the JSONL log files:

python scripts/cleanup.py

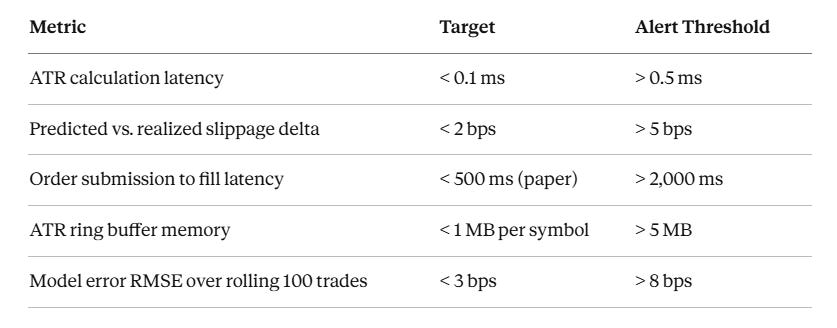

9. Production Metrics to Watch

These are the numbers you track in a rolling window on a deployed system. If any of them drift into the alert zone, stop and investigate before the next trading session.

The model error trend tells you whether your ATR_SCALAR calibration is drifting. If the model consistently underestimates realized slippage, the scalar is too low — recalibrate against recent fills. If it consistently overestimates, you may be passing on trades that would have been profitable.

10. Homework

Extend the slippage model to be regime-aware. The current version uses a single set of parameters for all market conditions. Here is what to build:

Classify the current market as

LOW,NORMAL, orHIGHvolatility based on ATR’s percentile rank over the last 20 sessions.Use separate

BASE_BPSandATR_SCALARvalues per regime. Calibrate them offline against historical fill data before using them live.In the

HIGHregime, add a position-size penalty: slippage scales with the square root oforder_quantity / average_daily_volume. Large orders in volatile conditions hurt significantly more than small ones.Emit a

REGIME_CHANGEevent to the terminal dashboard whenever the regime classification changes.

Deliverable: A filled order log from Alpaca paper trading showing regime classification, predicted slippage, and actual fill price for each trade. Your model RMSE over 50 consecutive trades must be below 5 bps.

11. Success Criterion — Day 60 Sign-Off

You pass this day when all three of the following conditions are true at the same time.

Condition 1 — Live order execution

Your data/orders.jsonl file contains at least one record where alpaca_order_id is a non-null UUID string, status is "FILLED", and fill_price is a positive float.

Verify it:

python -c "

import json

from pathlib import Path

records = [json.loads(l) for l in Path('data/orders.jsonl').read_text().splitlines() if l]

filled = [r for r in records if r['status'] == 'FILLED' and r.get('alpaca_order_id')]

print(f'Filled orders: {len(filled)}')

if filled:

print(f'Last order ID: {filled[-1][\"alpaca_order_id\"]}')

print(f'Fill price: {filled[-1][\"fill_price\"]}')

"

Condition 2 — Slippage within model bounds

For every FILLED record: predicted_slippage_bps must be between 3.0 and 50.0 bps, realized_slippage_bps must be between -10.0 and 50.0 bps (negative means price improvement, which is fine), and the absolute model error per trade must be below 15 bps.

The predicted slippage must vary across runs as ATR changes. If it is a constant 3.0 bps on every trade, the ATR feed is broken.

Condition 3 — Test suite green and stress test passing

pytest tests/test_atr_engine.py tests/test_slippage_model.py -v

# Zero failures, zero errors

python tests/stress_test.py

# [PASS] Stress test passed.

# p99 latency under 500µs

The terminal output that counts as a pass:

── Order Record ──────────────────────────────────

Alpaca Order ID : xxxxxxxx-xxxx-xxxx-xxxx-xxxxxxxxxxxx

Status : FILLED

Mid Price : 150.xxxx

ATR : 2.xxxx

Predicted Slip : 7.xx bps

Fill Price : 150.xxxx

Realized Slip : x.xx

Model Error : x.xx

Latency : xxx.x ms

All checks passed.

[PASS] Stress test passed.

A static 5 bps model always produces the same predicted cost regardless of what the market is doing. If your predicted slippage changes from session to session as ATR changes, the engine is working correctly. That is the point of today’s lesson.

Do not move on to Day 61 until all three conditions are met.