Quant Developer: Architecting Autonomous Trading Systems

Quant Python: Engineering Alpha with Code

Course Details:

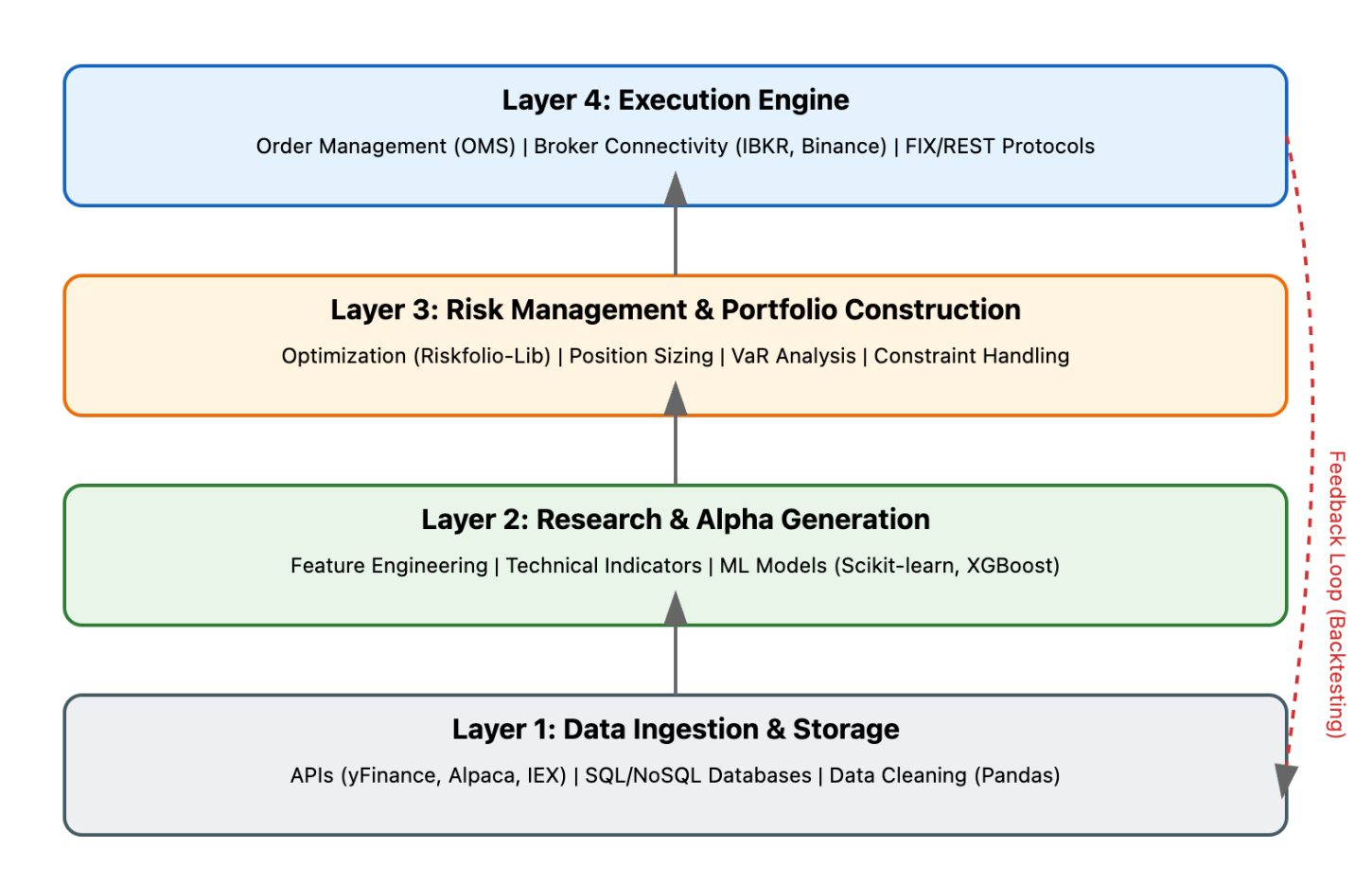

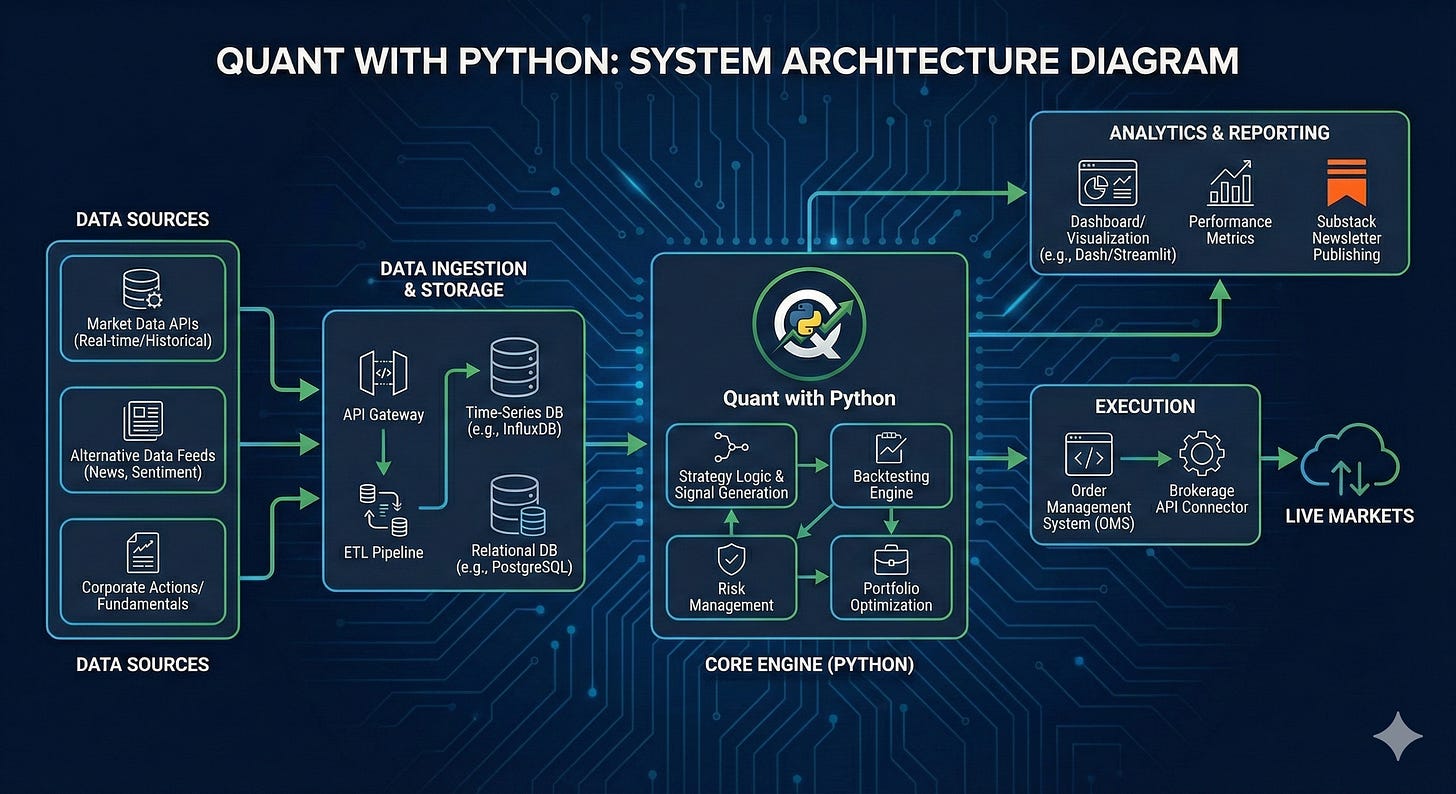

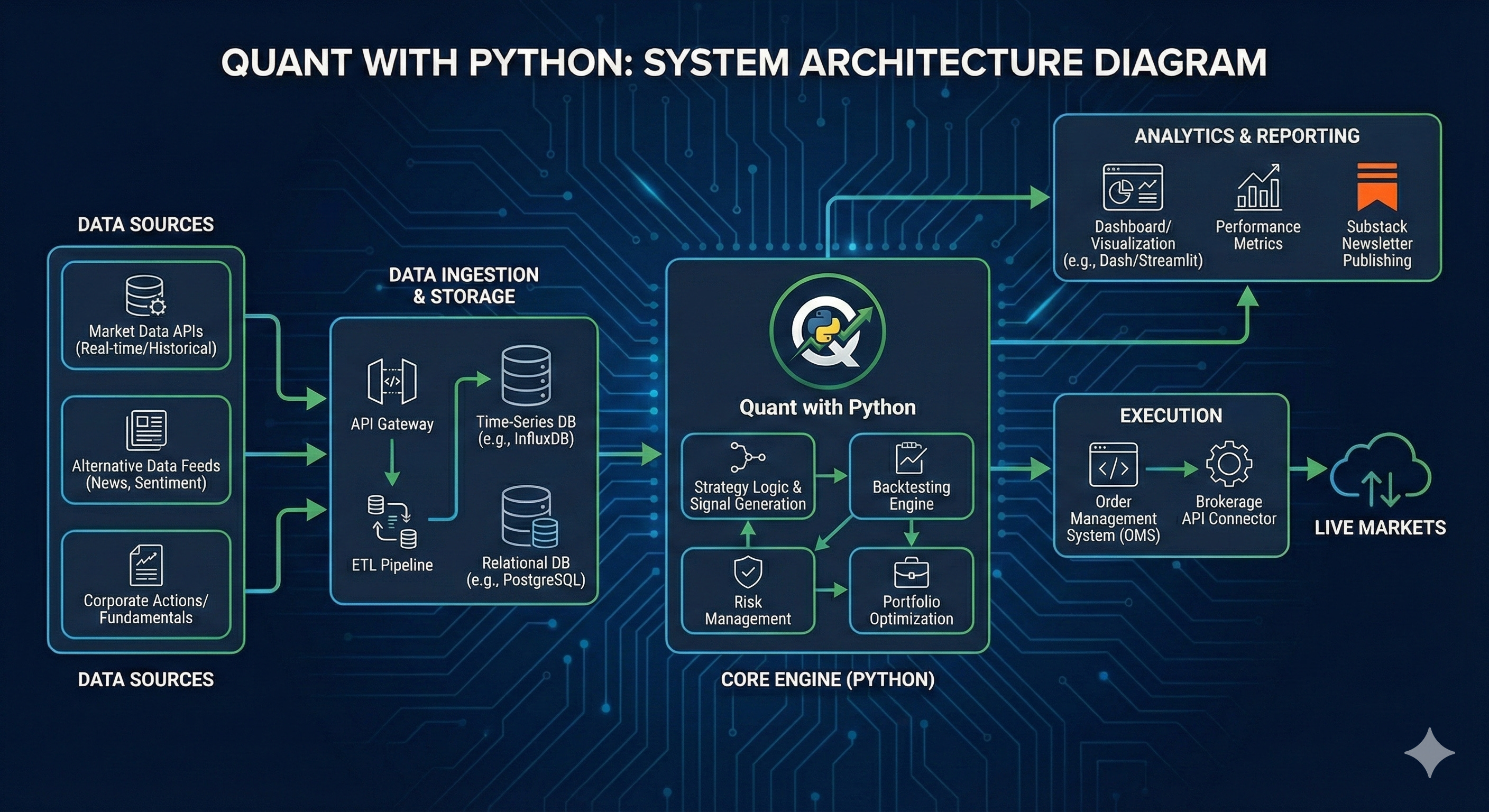

Why This Course? Most quantitative finance courses stop at backtesting on historical CSV files. In the real world, “backtest returns” don’t pay bills—execution does. This course bridges the gap between financial theory and production-grade engineering. You won’t just learn to calculate a Sharpe ratio; you will build a resilient, ultra-scalable execution engine that handles real-time WebSockets, manages risk autonomously, and deploys to the cloud.

What You’ll Build: You will architect an Autonomous Systematic Trading Platform. It features a multi-agent AI analyst, a vectorized research sandbox, and a real-time execution worker connected to the Alpaca Markets API. By Day 365, your system will be capable of fetching news sentiment, optimizing a portfolio of 50+ assets, and rebalancing trades without human intervention.

Who Should Take This Course?

Software engineers moving into Fintech, CS grads with a math bent, and system architects who want to understand the “low-latency” requirements of financial order books.

What Makes This Course Different? It follows a strict “One Day, One Codebase Change” rule. It prioritizes Event-Driven Architecture and Vectorized Computation over static data science. We move beyond the “Hello World” of finance into the “Hardening” of financial systems.

Key Topics Covered:

Phase 1: OOP Trading Abstractions & Numerical Backbones (NumPy/NumPy).

Phase 2: High-Performance Data Wrangling & Indicator Engineering (Pandas/TA-Lib).

Phase 3: Machine Learning Alphas & Modern Portfolio Optimization (skfolio/Riskfolio).

Phase 4: Live Execution, WebSockets, & Agentic Trading Workflows.

Prerequisites:

Basic Python proficiency (loops, functions) and high-school level linear algebra. No prior trading experience is required.

Course Structure:

A 365-lesson marathon divided into 12 “Sprints.” Every lesson includes a specific coding task, a system diagram, and a success criterion.

Curriculum: The 365-Day Roadmap

Phase 1: The Quant Stack & Financial Logic (Days 1–90)

Learning Objective: Translate mathematical financial formulas into reusable, object-oriented Python modules.

LessonTitleGoalLLM Generation Detail1–10Financial SyntaxCode fundamental calculators

Implement $FV = PV \times (1 + r)^n$ and CAGR logic.

11–25Logic & MarginAutomated risk alerts

Build a system that triggers “Margin Call” logic if $Equity < Margin\_Req$.

26–45Data StructuresSecurity metadata mapping

Use Python Dictionaries and NamedTuples to store Ticker, Sector, and P/E ratios.

46–65Error ResiliencyAPI Guardrails

Implement try-except wrappers for Alpha Vantage/yfinance to handle rate limits.

66–90OOP ArchitectureThe Broker Abstraction

Create a BaseBroker class and a MockBroker implementation with a submit_order() method.

Phase 2: Vectorized Research & Signal Engineering (Days 91–180)

Learning Objective: Master the “Mapmaker” (Pandas) and the “Backbone” (NumPy) to process millions of ticks instantly.

LessonTitleGoalLLM Generation Detail91–110NumPy MasteryVectorized Returns

Calculate log returns for 1,000 assets simultaneously without for-loops.

111–130Matrix MathCovariance calculation

Build a $N \times N$ correlation matrix for asset pairs.

131–150Pandas PipelineOHLCV Resampling

Resample 1-minute raw ticks into 15-minute and 1-hour candles.

151–165Indicator LabSignal Engineering

Use TA-Lib to code RSI, MACD, and Bollinger Band signals.

166–180Alpha DiscoveryMean Reversion Signal

Code a “Z-Score” indicator to find stocks deviating from their 30-day mean.

Phase 3: Validation, ML, & Portfolio Optimization (Days 181–270)

Learning Objective: Use statistical rigor to separate “Alpha” from “Noise” and optimize risk-adjusted returns.

LessonTitleGoalLLM Generation Detail181–200Backtesting LabEvent-Driven Simulation

Set up a Backtrader engine with realistic slippage and commission models.

201–215Strategy RigorWalk-Forward Analysis

Code a “train-test” split that advances through time to prevent overfitting.

216–230Machine LearningReturn Prediction

Build a Random Forest classifier in Scikit-Learn to predict next-day price direction.

231–245Alternative DataSentiment Scoring

Integrate news sentiment scores from the EODHD News API as a model feature.

246–260OptimizationThe Max Sharpe Portfolio

Use PyPortfolioOpt to find weights that maximize Return-per-Unit-Risk.

261–270Advanced ClustersHierarchical Risk Parity

Use skfolio to cluster assets by correlation to build a diversified portfolio.

Phase 4: Production Systems & Real-Time Execution (Days 271–365)

Learning Objective: Deploy an autonomous trading bot to a cloud environment with live telemetry.

LessonTitleGoalLLM Generation Detail271–285Alpaca APISandbox Connectivity

Authenticate alpaca-py and fetch real-time “Paper Trading” account status.

286–300Order MgmtBracket & Limit Orders

Submit multi-leg orders (Entry + Stop Loss + Take Profit) programmatically.

301–320Live TelemetryWebSockets Stream

Build an asyncio listener for real-time price ticks from Alpaca’s stream.

321–340Cloud OpsAWS EC2 Deployment

Dockerize your bot and deploy it as a systemd background service on Linux.

341–355MonitoringTelemetry & Alerts

Build a Streamlit dashboard or Slack bot to report daily P&L and trade logs.

356–365Agentic WorkflowsAutonomous Analyst

Connect an LLM (via MCP) to generate a macro summary before market open.

LLM Lesson Generation Prompt

Use this prompt daily to generate the specific “Hands-On” content for your current lesson.

System Prompt: “You are a Senior Quant Developer at a top-tier fintech firm. Provide Day [X] of the ‘365-Day Quant Developer’ course.

Goal:.

Constraint: Ensure the lesson is 100% hands-on.

Requirements:

Provide a Mermaid.js Diagram (Flowchart or Class Diagram) showing the system architecture.

Provide production-grade Python Code using modern libraries (e.g.,

alpaca-py,pandas,skfolio).Explain the ‘Why’ behind the implementation (e.g., why use WebSockets over REST?).

End with a Success Criterion (e.g., ‘Your code should print a valid Order ID from the Alpaca Sandbox’).

Tone: Professional, mentor-like, avoiding clichés.”

Key Learning Objectives:

Architecture: Design event-driven systems that react to market events in $<100ms$.

Engineering: Build data pipelines that handle missing ticks and handle API rate limits gracefully.

Strategy: Distinguish between “curve-fitting” and statistically significant alpha factors.

Production: Manage live capital (or paper trading) using robust error handling and cloud infrastructure.